The world has never seen as much change and adjustment as it did in 2020, where companies were forced to pivot rapidly and adapt to challenges brought on by the global pandemic. The lockdowns and shutdowns unfortunately extended too long for many businesses, for others their technology platform wasn’t ready, or they were in an industry where it was too difficult to fully adjust to rapidly emerging business requirements. Collaboration tools such as relative newcomer Zoom along with Microsoft Teams, Google Meet, WebEx, Slack, and several others flourished as they allowed us all to work from home, while more and more organizations kicked off their delayed Digital Transformation or general cloud plans. Behind much of this change in business was Consumers – they shifted and shifted quickly. Pandemic restrictions and working from home meant everyone started to shop online for curbside pickup or home delivery. Many used technology platforms they were already familiar with like Amazon, Netflix, Doordash and their online banking tools, and as the graph below shows, online e-commerce businesses did really well. The American market likely differs from the experience in other countries but it shows a significant jump in online sales in the largest economy on earth.

Retail e-commerce sales in the US market increased drastically in 2020. The total e-commerce sales for 2020 were estimated at $791.7 billion, an increase of 32.4% from 2019. (Source: US Census Bureau News)

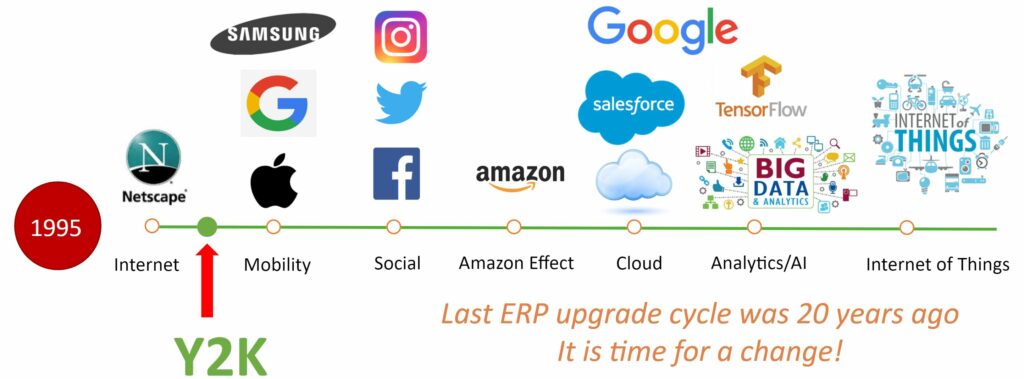

This also meant a significant shift for businesses. While the cloud providers initially were offering Infrastructure as a Service (IaaS) and Software as a Service (SaaS), they are now rapidly expanding in the Platform as a Service (PaaS) space. It is not only the ERP providers such as Microsoft, SAP, Oracle, and Infor, but we see also Google Cloud and Amazon Web Services entering the space. While the last two are not likely to develop an ERP, they will use their infrastructure, solutions, tools and general reach to engage with businesses they are not working with yet and attract more business users to their clouds through industrial cloud and business apps. This gives business users the opportunity to select and use best-of-breed solutions offered by a fast growing variety of tested and approved providers. The same way we download our favorite apps on our phones for our specific personal use, the use of industry specific business apps will reduce the complexity of business software implementations. This also introduces further changes in the implementation landscape where a shift to Consulting as a Service (CaaS) is already under way.

In addition to a reduction in overall services, some larger system integrators have begun to offer their ERP and CRM implementation services as a subscription model, the same way as some made for cloud ERP providers are offering, and effectively turning the typical CapEx for implementation services into an OpEx for the customers. Large consulting and system integrator firms with deep pockets are financially much better positioned to transition to this model. For the medium and smaller players, it will become more difficult to hang on while bankrolling and adjusting again to another revenue model.